Cooking up a housing bull BBQ – Christopher Joye

[ad_1]

In the AFR I generate that back again in early 2020, this column dusted off its double-barrel “shottie” and went looking housing bears, which were being confidently roaming everywhere you go. When it was seemingly mission impossible—one lonely, albeit daring, bull surrounded by “hangry” grizzlies salivating around 10-30 for every cent house price falls (if not more)—it in the long run proved to be a one-sided massacre. A bear blood-bathtub, if you will.

This column argued selling prices would only tumble -5 per cent (they drop 2 per cent) amongst March and September 2020, next which they would spike as much as 20 for each cent, which we subsequently revised to 25-30 for every cent. In the final evaluation, Aussie property owners banked cash gains well worth 29 for every cent.

Rapidly ahead to Oct 2021, and this weary bear hunter declared that the cross-hairs had been likely to be turned on the hordes of rabid housing bulls, who ended up now triumphantly roaming the serious estate savannah, bloated on record rates. It was time to chow down on a juicy “bull BBQ”.

Particularly, we predicted that countrywide dwelling values would climb at minimum another 5 for each cent (they are up 5.4 for every cent) ahead of suffering a record 15-25 per cent slump following the initially 100 basis details of RBA price will increase. It was anticipated that the RBA would kick-off this system in mid 2022 at the earliest.

The universally bearish retail and expenditure financial institutions, which experienced been pressured by the cost action in 2020 and 2021 to embrace our bullish sights, had seemingly learnt their lesson this time all around. In just a couple of months of our October proclamation, most financial institutions had swung 180 levels, quickly projecting sharp value falls (although none as savage as our 15-25 per cent attract-down).

That all adjusted on Friday when Australia’s most significant financial institution, CBA, folded, last but not least calling for a national peak-to-trough drop of 15 per cent as a consequence of the RBA’s aggressive tightening cycle.

Specified the banks’ swift mistake correction, tasty bulls have, in reality, been comparatively challenging to sight given that late last year. To be certain, there are however a few solitary beasts peddling the preposterous strategy that residence prices will not drop as borrowers’ getting ability plummets care of a large rise in house loan rates.

What the RBA giveth, it now taketh absent. Slashing its funds price from 1.5 for each cent to .1 per cent between June 2019 and November 2020 boosted Aussie property charges by 37 percentage points. A prudent person should now suppose that significantly of this wealth generation is paid out-again.

Regardless of Martin Position not getting able to properly forecast its subsequent foot-action, it someway has conviction that the dollars amount really should climb to what it judges to be a “neutral” amount close to 2.5 per cent. The fact is the RBA has zero clue exactly where neutral essentially lies, and would be well served by some humility on this front.

For insane-brave housing bulls and dwelling homeowners throughout the region, the scary factor is that our forecast for a 15-25 for every cent decline in national prices was predicated on the RBA lifting its income price by at the very least 100 foundation factors. And but the recent prepare, in accordance to Governor Phil Lowe, is to leap to 250 foundation details. We have not unveiled what we imagine will happen to dwelling prices if the discounted variable property finance loan amount does in fact elevate from circa 2.25 per cent in April 2022 to 4.75 for every cent subsequent 12 months.

Traders like to convenience on their own with the encounter of the Reserve Financial institution of New Zealand, where by Governor Adrian Orr has led the globe in jacking-up his money amount from .25 for every cent in September 2021 to 2. per cent now.

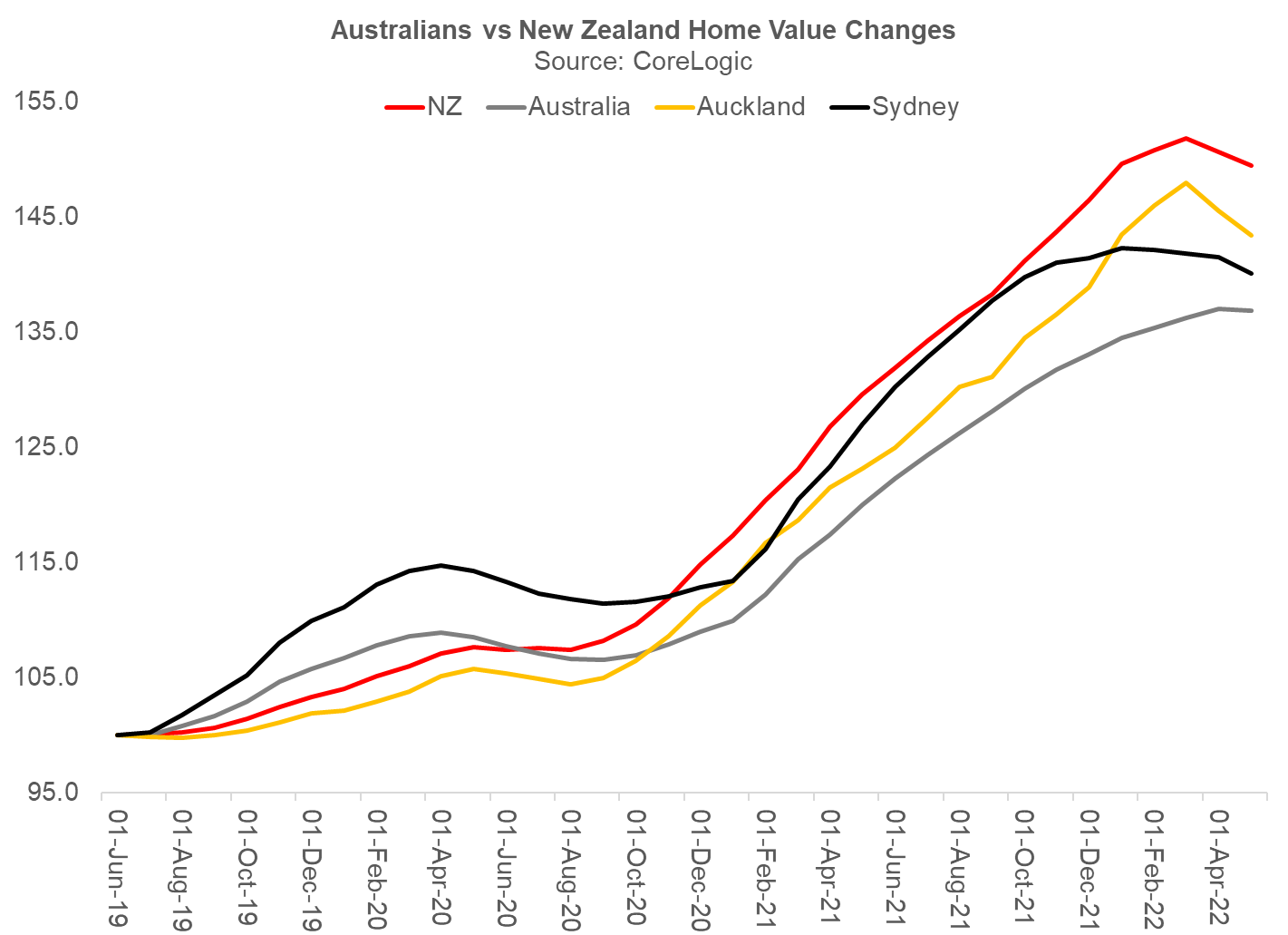

The market myth goes that notwithstanding that New Zealand household selling prices have crashed, the RBNZ just keeps on lifting. This is finish BS. The RBNZ’s formal household price tag index is a sequence generated by CoreLogic, which also publishes Australia’s leading dwelling benefit benchmarks.

It turns out that NZ dwelling values have barely moved in the encounter of 175 basis details of fee will increase. From their peak in March 2022, NZ selling prices have only declined 1.6 per cent. (Other unofficial indices put the correction at a a little bit larger 3 for every cent.) NZ’s biggest city, Auckland, has worn cost falls of only 3.1 per cent so far.

Without a doubt, it is apparent the Sydney housing sector began rolling above in early 2022, in advance of its NZ counterparts. It is also obvious that Aussie residence rates are a lot more sensitive to rate adjustments.

Whereas the RBNZ commenced lifting prices back again in Oct 2021, the RBA only kicked-off in May well this calendar year. And nonetheless Sydney price ranges are previously down 2 for every cent with Melbourne (off 1 for each cent) next carefully guiding.

A vital variation is that while 88 for each cent of NZ property financial loans are mounted-costs, and consequently insensitive to RBNZ improves, most Aussie house financial loans are variable-charge. The majority of Aussie debtors have been accordingly whacked by a 50 foundation position maximize in their month-to-month curiosity invoice when the RBA shipped a double-whammy this thirty day period.

The mythology of the RBNZ bravely raising charges in the face of substantial household value falls is just a fairy-tale.

For the foreseeable long term, however, the RBA is going to be racing in the direction of its terminal money charge, which bond markets are at the moment pricing at close to 4 for every cent. Visualize that, discounted variable mortgage rates climbing to 6.5 per cent!

This is nonetheless throwing up some quite exciting and strange opportunities. Look at NAB’s most up-to-date hybrid situation (NABPI), which attracted far more than $3.1 billion in trader demand (NAB issued $2 billion). NAB is shelling out a 3.15 per cent money margin over the quarterly lender bill swap level, which is 1.5 for every cent. That suggests investors will be choosing up a 4.65 for each cent annual operating produce on the new NABPI hybrid.

However if we take into consideration the anticipated yield around the lifetime of this 7.5 yr hybrid, which accounts for the market’s projection for the RBA funds level climbing to 4 per cent, the generate to maturity (or generate to its expected reimbursement day) is 6.95 for every cent.

That indicates that NABPI’s produce to maturity of circa 7 per cent is virtually identical to the franked dividend generate shareholders gain on NAB’s equity, which is also 7 for every cent. And it is higher than the 6 per cent franked yield you get on Aussie equities, which is just one explanation why we also bought it.

Main lender hybrids have historically experienced about 1-quarter of the volatility of major lender shares. And they have also outperformed for the duration of shocks: when the pandemic initial hit in March 2020, NAB’s shares fell 34 for each cent. In distinction, the significant lender hybrid index only lost 6.3 for every cent in that thirty day period.

Another case in point of unusually desirable income returns was Macquarie Bank’s lately issued 5-year Tier 2 bond, which compensated a generate of 6.1 for every cent. We bought it mainly because we do not think the RBA will get near to a 4 per cent funds rate.

Irrespective of whether that arrives to move will count a lot on what transpires to Aussie dwelling charges, which are a person of the purest representations of the RBA’s financial coverage transmission system. It is pretty challenging to picture Australia will have any inflation difficulty when property rates have fallen by a lot more than 15-25 for every cent…

Obtain Coolabah’s mental edge

With the most important staff in financial commitment-grade Australian preset-money and above $7 billion in FUM, Coolabah Cash Investments publishes distinctive insights and research on marketplaces and macroeconomics from all-around the entire world overlaid leveraging its 14 analysts and 5 portfolio managers. Click on the ‘CONTACT’ button below to get in contact.

[ad_2]

Supply url